Consumer credit insurance – fact sheet

What is it?

If you have taken out a loan recently, or you have a credit card, the finance provider might also have sold you consumer credit insurance.

Consumer credit insurance (CCI) is sometimes called Loan Protection Insurance, Mortgage Protection Insurance, Credit Card Insurance or Personal Loan Insurance. It provides some cover if you can no longer afford to meet your credit repayments in some circumstances.

There are different types of cover available, but they are generally made up of:

- Disablement (for if you cannot work due to illness or injury)

- Unemployment (for if you lose your job unexpectedly)

- Life (for if you pass away)

Some policies also have cover for trauma (which can provide cover if you suffer a ‘trauma’ for example, cancer or a stroke) or terminal illness (which can provide cover if you suffer a terminal illness).

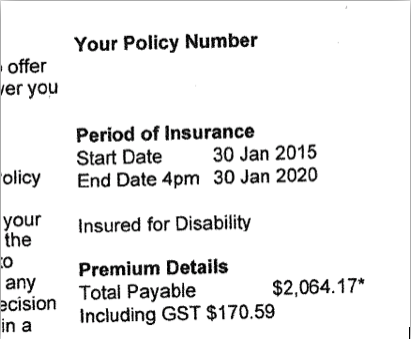

If you have CCI, it will probably cover one or more of the above parts. They should be set out in your certificate of insurance. This is the letter the insurer sends you listing the details of the insurance personal to you, for example the price and the options you have chosen. It usually has your name and address on the top left hand side.

This person has bought disability cover only:

You can ask your insurer for a copy of the certificate of insurance and the policy wording if you cannot find your copy. You can also ask your insurer what cover you have if you can’t work it out from the documents.

What’s the problem?

These are some of the issues we see:

- It might be useless to you. For example, unemployment cover in a CCI policy will probably not pay out if you are unemployed or working on a casual basis.

- Premiums are quite expensive. Expect to pay over $2000 for CCI. Remember that if you’ve paid for the insurance with a loan, you’re also paying interest on that amount. To see how this works in practice, read about Consumer Action’s client’s experience here.

- Payments might not cover the full amount of debt. For example, if you become unemployed or disabled, the CCI may only cover your repayments for a certain period of time. CCI may only pay minimum monthly repayments on a credit card, not the rest of the debt.

- A tricky sales process. A salesperson will sometimes add CCI onto a loan or credit card without explaining what the CCI is, or without the customer even knowing they are buying it.

What should you do?

Step 1: Check your policy to see what it covers or doesn’t cover and whether it is what you thought it was. Check out our fact sheet here to help you work this out.

Step 2: Think back on when you were sold the insurance. Did you agree to buy this insurance or was it just bundled in with other papers when you got a loan or credit card? Did you feel pressured to buy it? Were you given any incorrect information? Was the process unfair in any other way?

Step 3: If this insurance was added onto your loan without you knowing, the salesperson lied about the insurance or you think you were treated unfairly, you might be entitled to get a refund. You can use our template letter here.

Want more information?

The ASIC Money Smart website has really helpful information about consumer credit insurance.

If you want to read more about problems Australians have experienced with these products, have a look at Consumer Action Law Centre’s report, ‘Junk Merchants’ available here.

This fact sheet is for information purposes only and should not be relied upon as legal advice. This was updated on December 14, 2015.